15th August, 2015

1. So far the attack on tax avoidance was Unilateral - Government of India attacking all kinds of tax planning. Now the attack is “Multilateral”. It means attack from several fronts, in several manners. Some attacks are already incorporated in law. Some are at discussion stage.

“All Tax Payers are equal. But some are more equal than others”.

With apologies to George Orwell. His famous Book “Animal Farm” shows how authorities create distinctions for themselves; and how the concept - “Equality before Law” is a mere academic concept.

This paper is in addition to three other papers written on the same subject - Click here

1.2 Attack on Black Money: Elaboration:

Indian Government has started a serious attack on: (i) Tax Avoidance (or Tax Planning) & (ii) Tax Evasion. Both the attacks together are considerably stronger than any attempt at unearthing black money in the past.

1.2.1 Attack on Tax Avoidance:

The first serious attack under the present Government is on tax planning by creation of SPVs (Special Purpose Vehicles) outside India. Indian residents incorporate companies in tax havens. These companies then conduct business abroad or hold properties/ investments abroad. Under the Income-tax Act 1961, all these incomes and assets were exempt from Indian taxes.

The Government knew about it for many years. In the Direct Taxes Code (DTC), it was proposed to change the definition of a company’s residential status. This proposal of DTC has been accepted. Now a foreign company will be treated as Indian resident if its “ Place of Effective Management” (POEM) is situated in India. The term POEM is similar to “Control & Management”. However, there are some fine differences.

Indians have formed thousands of SPVs in tax havens. Most of these SPVs will be considered as Indian Residents under POEM rules. If they do not disclose their incomes in the assessment year 2016-17; Black Money Law will apply. Harsh consequences can result. Once a foreign company is treated as Indian resident, its Global Income is liable to Indian tax. It is also liable to Tax Audit, Transfer Pricing audit, TDS provisions, etc.

Apart from POEM, following attacks have already been incorporated in the Income-tax Act (ITA). Transfer Pricing provisions; Taxing Indirect Transfers; and several deeming provisions under S.9. Further provisions to come into effect will be: GAAR & CFC.

BEPS reports will be announced at the end of year 2015. Then Government of India is committed to make further amendments in law appropriately.

1.2.2 Tax evasion:

This is the most serious attack. Following is the list of laws that Government of India has enacted or modified to attack the black money.

(i) Black Money Law: The new law has been passed under the title “The Black Money (Undisclosed Foreign Income and Assets) And Imposition of Tax Bill, 2015”. This law is in response to BJP’s election promise to bring back black money held abroad. It provides for tax, penalty & prosecution. It has created serious fear in the minds of many persons including politicians having assets abroad.

The law offers a Voluntary Compliance Scheme (VCS) as an opportunity to voluntarily comply with the law. Those who are caught violating the law are threatened with harsh consequences.

(ii) Foreign Exchange Management Act (FEMA): Finance Act, 2015 has introduced Sections 13 (1A) to (1D); and Section 37A in FEMA. The provisions will be to confiscate Indian assets of equivalent value for any assets held abroad in violation of Section 4 of FEMA. These amendments also provide for penalty and prosecution.

(iii) Prevention of Money Laundering Act (PMLA): This law also makes it a scheduled offense if an assessee evades tax etc. payable under the BML.

(iv) Benami Transactions (Prohibition) Act.

1.2.3 Global Attack on Black Money:

(i) BEPS: This time, Government of India is not alone in its attack on black money. USA, UK, Germany, France; OECD, G20, EU – and other countries and Groups are making a concerted attack on black money. At the instructions of G20, OECD is working on “Base Erosion & Profit Shifting” (BEPS) project. It has targeted fifteen action plans. The final reports will be published in November, 2015. Then G20 countries are committed to bring appropriate laws to curb tax avoidance & tax evasion.

Double Non-Taxation: In academic conferences and even before Courts of Law, we had eloquent arguments justifying Double Non-Taxation. FIIs and companies like Hutchison – Vodafone have escaped double non-taxation and media has widely supported it. BEPS is a direct and frontal attack on Double Non-Taxation. Simultaneously several country laws and Double Tax Avoidance Agreements/ commentaries will be amended to disallow double non-taxation.

(ii) More than sixty countries associating together have entered into multilateral agreement for “ Automatic, Simultaneous Exchange of Information”. These include most prominent Tax Havens also. These Governments will share information on tax avoidance & tax evasion.

(iii) Financial Action Task Force (FATF) and Financial Intelligence Units (FIUs) are formed by several countries and they are cooperating with each other in sharing information. These are primarily to deal with drug & terror money. However, incidentally, they have been important source of information for black money.

Under the PMLA, global banks and financial institutions have been instructed to track and report all suspicious movements of funds. When any movement is considered suspicious, it gets automatically reported to the FIU of the relevant country. This movement has caused maximum pressure on movement of funds within tax havens. People, who have earlier held black money in tax havens, now find it difficult even to move the funds from one tax haven to another or to return the funds from abroad to India.

This attack is through the banking system. In a computerised world, a transaction between two persons in Switzerland & Mauritius can be tracked at New York & reported to New Delhi. This was not possible earlier. Now it is possible. This is how Hasanali Khan’s case came to light.

Tax Haven Governments & banks are on the firing line.

(iv) Banking Secrecy: Under the leadership of US Government & OECD, Several Governments are forcing the tax havens including Switzerland to open up their secret records and get the information on black money. The stand taken by these tax havens that their domestic laws don’t permit sharing of information is not accepted by global Governments. Banking Secrecy is being demolished with strong blows.

All these actions together will substantially change International Tax Practice. Tax havens will be hurt. Old Tax Planning structures are no longer profitable. Dismantling them can also invite substantial taxes.

1.3 Micro & Macro Approaches:

How do we study a law? Micro approach: Take a section. Study. Interprete. See how you will argue before the AO/ Court. This paper is designed to have a macro look at the Attack on Black Money. Hence let us examine the applicable laws from a macro angle.

What is the difference between – (i) Narrow interpretation or micro approach; & (ii) Macro View?

Compare with illustration:

A new-comer is searching for a home in the streets of Old Delhi. He is wandering from one street to another. Not sure about which is the right street. This is narrow interpretation.

Another man has Google map on his phone. He takes an aerial view of the area, knows where the house is located and then goes for the address. The aerial view is macro view.

1.4 Macro Angle is:

“My client should not come into difficulties from any angle. His assessments should, in principle, be completed at AO level”.

“How do I ensure this?”

By making him aware of all the aspects of: “Attack on Black Money”.

1.5 The international scene has changed significantly after the American financial crisis that erupted in the year 2008 with insolvency of “Lehman Brothers”. Indian scene has changed significantly after the change in Government in May, 2014.

1.6 Counter View: “All Tax payers are equal…..but some are more equal than others.” They will not be affected even under the harsh Black money Law.

1.6.1 Jain Hawala Case, Telgi Stamp Paper scandal, Hasanali Khan case – in all cases Politicians of different parties were involved. Which politician has been punished?

1.6.2 FII. MAT (Please see 1.1.D above.)

On 28th February, 2015 the Finance Minister presented budget & proposed relief from MAT for FIIs – with prospective effect. FIIs raised a hue & cry & claimed benefit with retrospective effect. On 6th April, Mr. Arun Jaitley made a formal statement: “India is not a Tax Haven. You can’t avoid paying all taxes.”

In May, Mr. Arun Jaitley agreed to reconsider the issue. First the relief was announced to FIIs coming from DTA countries. Now even non-DTA investors are

being considered by a committee headed by

Justice Mr. A. P. Shah. What made Finance Minister take an about turn?

Paragraph 1 – “Macro View” completed.

2. FEMA :

2.1 Basic Understanding in Short:

Even after all the liberalisations, an Indian Resident cannot do following transactions unless and until he is permitted to do so – (i) by some notification or circular; or (ii) by a specific permission given by RBI.

Section 3 of FEMA prohibits all Indian residents from making any payment to a Non-Resident.

Section 4 – No Indian Resident can hold any assets outside India.

Section 8 – if an Indian Resident is entitled to receive any assets outside India, he is bound to bring the same to India.

Now Finance Act 2015 has introduced two new provisions in FEMA. Intention is to bring back Indian black money held abroad.

2.2 FEMA – S.37 A. Enforcement:

This provision is to enforce the person into bringing to India his black money held abroad. Consider the section:

Extracts: If the Enforcement Officer

SUSPECTS that

a foreign asset is held in violation of S.4 of FEMA, he can seize assets in India of equivalent value. He shall record the reasons in writing.

Implications:

(i) An enforcement officer needs to only suspect. No evidence required. No notice to be given. Just go ahead and seize assets.

(ii) Identity of the owner of foreign assets; and identity of the owner of Indian assets – do not have to be established or linked. If he suspects that Foreign Assets are held in violation of FEMA; can he go ahead and seize in India – any one’s any asset?

This law is without reasonable protection for the citizens of India; is arbitrary; and has unacceptably harsh implications. It needs to be struck down at the earliest.

2.3 Section 13 (1A): Penalty & Enforcement:

Kindly separate each phrase of the section and then read.

First phrase is cause of action.

Subsequent phrases are consequences.

First Phrase: Cause of Action:

“ If any person is found to have acquired ….”.

(Note: Simple words are “have acquired”. There is no qualification that “acquired in violation of FEMA”.)

“Foreign assets

situated outside India

exceeding limits prescribed u/s. 37A(1).”

Second Phrase: Consequences:

(i) “He shall be liable to a penalty of up to three times …..”

the sum involved –

..... in such contravention.”

(Note: the word “such” means that there is a preceding reference to a contravention. However, the preceding phrase simply refers to acquisition of foreign assets. There is no mention of any violation of law. A clear case of bad drafting of law.)

A fair and hence correct interpretation of law would be: If the original acquisition of the asset was in violation of FEMA, then only S.13 (1A) will apply.

(ii) “And confiscation of value equivalent ….”

(Again grammar fails. Value equivalent to what? The word “to” is missing. Because the sentence is so structured that it is difficult to place the word “to”.) Held / owned by whom?

For example, TISCO & TELCO have acquired shares in CORUS. Can the Enforcement Officer seize the assets of Mr. Ratan

Tata or

Mr. Cyrus Mistry? (Please see paragraph 2.2(ii) above.) This illustration seems outlandish. However, the way, the law is drafted; this can be an

interpretation of the law.

Hindustan Aluminium (HINDALCO) has acquired shares in a Canadian Company Novellis at an all cash price of $ 6 billion in the year 2006. It was being debated that Hindalco has paid an excessive price. This can be an alleged violation of FEMA. Enough suspicion. Enforcement Officer need not issue any notice. He can go ahead and confiscate the foreign asset; and then impose a penalty of upto $ 18 billion.

Note: Under FEMA, there is NO time limit upto which the Enforcement Officer can take action. FEMA became operative on 1st June, 2000. So the enforcement officer cannot go to a date prior to 1st June, 2000.

Comment: When an officer is given arbitrary powers, someone somewhere is bound to abuse those powers. In Hindalco’s own case, we have seen arbitrary decisions passed by Transfer Pricing Officer: “Guarantee given by Hindalco for loans taken by Novellis.”

Observations: Hindalco will fight such arbitrary actions in a Court of Law. Can everyone afford going to Court?

2.4 FEMA: S.37 A & 13 (1A) – Combined effect:

Are both the sections cumulative or complementary? In other words, for a suspected offence of $ 100 under FEMA, can the Enforcement Officer –

(i) Confiscate Indian property worth $ 100 u/s. 13 (1A); and

(ii) Seize Indian property worth $ 100 u/s. 37A(1)?

Both sections are drafted as if they are separate.

2.5 Combined effect of FEMA & BML:

When a person transfers his black money outside India by Hawala; he violates both – ITA & FEMA. What will be the combined effect of the penalties under both the laws? Apart from penalties and seizure of assets; can there be prosecutions under both the laws?

Illustration:

Mr. IR, an Indian Resident sent abroad Rs. 10 lakhs by hawala when the exchange rate was Rs. 50 = 1 $. He got $ 20,000. On

1st July, 2015, the AO gets this information. Current rate is say Rs. 65 and value of the foreign undisclosed asset is Rs. 13 lakhs.

Clear case of punishment completely disproportionate to offenses committed. Under the constitution, there have been decisions – many decades back; that penalty for any offense has to be commensurate with the gravity of the offense. Today, it seems, such principles of civilised democracy are given a burial – together with the burial of “equality before the law”. One may make a risk analysis before embarking on any black money transaction.

If the asset is brought back into India, seizure can be set aside – S.37A. So bring the assets, pay up the tax and reduce penal action by 100% of black money.

2.6 Consider the practical difficulties.

(i) Mr. IR remitted $ 2,50,000 under LRS and incorporated a company in the UAE. The company purchased an apartment in UAE worth

$ 2,45,000.

(ii) In the year 2010 RBI decided that IR could not have incorporated a foreign company under LRS. Hence the shares held by IR would be a violation of S.4 of FEMA. RBI did not issue any circular or notification. Just started taking action against such investors.

(iii) RBI continues to behave in such arbitrary manner in many matters with no scope for appeals.

(iv) When RBI says, something is a violation of FEMA; Enforcement officers accept it as a conclusive evidence of violation and take further action.

Now, countless innocent Indian residents are exposed before a draconian law – FEMA. Their exposure is more vulnerable because of arbitrary behaviour by RBI.

Note: RBI is the most respected institution in India today. Hence my statement may not be palatable for many. But those who have suffered on account of LRS investments, may appreciate this statement.

2.7 In the year 2000, FERA, a Criminal Law was replaced by FEMA, a civil law. The power to prosecute was taken away. Now FEMA has become a criminal law. Prosecution is back. FEMA is back to FERA stage.

A draconian law bound to cause more harm than good. Can high value corruption and harassment be far behind?

You decide: Do we have a civilised democracy in India?

FERA was an absolute law. Very harsh. Contrary to Business Logic. No one could win in an appeal in a Court of Law.

And it completely failed.

[This is a radical statement and can take one hour discussion. Suffice it to say that: (i) Law makers themselves used hawala system on a large scale; and (ii) Anyone could transfer black money in either direction at Will.]

2.8 My submission: When a law is too harsh; and Even courts have little jurisdiction - The law fails. When harsh & arbitrary powers are given to any authority, some officers will harass the small & medium businessman and corruption will be rampant. The slogan of “Ease of doing business in India” goes for a toss. India has experienced this phenomenon for many decades. In such a situation, the spirit of free enterprise will die. Fair competition will take a back seat. Corrupt businessmen will flourish. Indian GDP growth rate will go back to 2% per year.

We hope, all my apprehensions prove to be false.

3. Reason for the Attack on Tax Evasion & Tax Avoidance:

Let us see a few Tax Avoidance games with the help of some charts.

Charts:

Chart 1

Alleged Route employed by some share market manipulators

in the years 1991-92.

When Azadi Bachao Andolan (An NGO) challenged India – Mauritius DTA, Government of India put up all the fight to protect the DTA.

Black Money Routing: Chart I – Explanations.

Share market speculator had real ownership of Mauritius companies that speculated in the Indian share market. He held those companies through Benami NRIs & manipulated share market.

Even in those years, more than a thousand cases were filed by several regulators against the share market speculators.

Under the current regime, holding assets abroad is a violation of – Tax laws, FEMA & Benami Transaction Law. Now add BML. SEBI and related laws have their own consequences.

These brokers acted individually and faced harsh consequences. Compare their fate with FIIs in Chart 3.

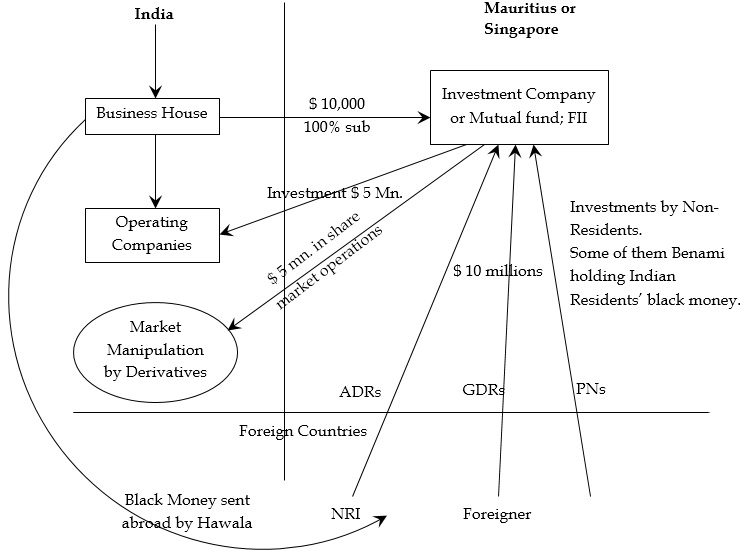

Alleged Black Money Routing by

Business Houses

Chart 2

All these ADRs, GDRs, PNs are Financial Interest/ Assets. Some of them are Indian Residents’ black money held abroad Benami and used for financing business & financing share market operations. They abuse DTA and get tax free profits to manipulate markets. These are violations of FEMA, ITA, Benami Transactions Law & BML.

Chart 3

An Alleged Route of Money Laundering

Notes:

1. SEBI, RBI, Ram Jethamalani & Supreme Court – all have raised voices at different times. It is rumoured that PNs are used to launder black money into India. A provision has been made that while FIIs have to obtain KYC for the investors, it will have to disclose only if & when the regulators enquire in specific cases. There have been cases where FIIs have not disclosed information to SEBI & instead agreed to pay penalties.

2. If anyone has conducted this transaction, it was a violation of FEMA even before amendment. After amendment, it is exposed to seizure and violator is exposed to prosecution.

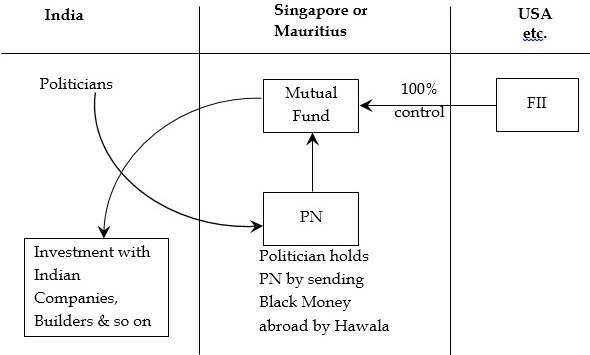

3. When a politician does this series of transactions, it becomes a PMLA violation also.

It is of course a tax violation.

4. Now under BML, the FII can also be prosecuted.

Also, the tax consultant can be prosecuted.

5. However, in India FIIs have tremendous influence. All Governments pass laws specifically suitable to FIIs. Latest amendment made by the present Government is to treat FII assets as Capital Assets. S.2 (14) of the ITA. The tax benefits they get is a subject beyond the scope of present paper.

6. How and why have India and the world come to such a sorry state of affairs? Some powerful business houses, large MNCs and politicians resort to several strategies for tax avoidance & evasion. Regulators feel helpless & frustrated. So they want more powers. They don’t realise that when the bosses decide to break the law, regulators can’t do anything. The vicious cycle of tax evasion/avoidance –more powers for the Regulator – new loopholes – ultimately results into a legal system that fails. This happens in most countries – India is not unique.

Notes to Para 3 – Charts - Completed.

4. Prevention of Money Laundering Act (PMLA):

4.1 Confiscation of Indian Property:

Finance Act has introduced a new concept under FEMA. Indian residents may have black money held abroad through tax haven countries and tax haven banks. When the Government demands return of those funds, the tax havens may not co-operate. Government’s move may be frustrated. In such a situation, the Enforcement Officer is authorised to confiscate Indian assets equivalent in value to the foreign undisclosed assets.

This concept is brought into PMLA vide Section 2 (1) (u) by amending the definition of Proceeds of Crime (POC). Section 5 of PMLA authorises Enforcement Officer to attach POC. Under Section 8 (5), the POC may be confiscated. Thus now, assets in India equivalent in value to POC located outside India can be attached and confiscated.

Note: Confiscation/ seizure under FEMA is for FEMA violation. In law, there is no link between tax evasion and confiscation under FEMA. Similarly confiscation under PMLA is only for PMLA violations.

4.2 Tax violation included under PMLA:

Section 88 of BML makes an addition to the list of scheduled offences under PMLA. “Willful attempt to evade any tax, penalty or interest payable under BML” now is a scheduled offence under PMLA. And then there are powers to confiscate property.

Who will have this power? Not the Income-tax department. It will be the Enforcement Department under PMLA. This will be in addition to the powers under BML for prosecution of the assessee.

DOE had seriously tried in the nineties to get a power to act on tax evasion. So far it was not granted. Now DOE has succeeded in getting that power. DOE to act for tax evasion not involving any money laundering crimes. Businessmen are exposed to even more risks.

5. Miscellaneous Provisions:

5.1 Gold Monetisation Scheme

5.1.1 Banks will take deposit of gold from public.

Banks will lend this gold to Jewellers.

or sell gold for their own needs of CRR/ SLR/Foreign exchange.

Who will bear the price fluctuations? Banks.

Who will bear the risk of Bad Debts? Banks.

5.1.2 Following factors advise against trusting anyone for gold:

(i) Wild fluctuations in gold price per US ounce - $ 400 - $ 600 - $ 1900 to $ 1200.

(ii) Huge losses suffered by U.S. Government & Banking Cartel.

(iii) Huge derivatives trading in gold.

5.1.3 My personal view – “Gold is my reserve for unforeseen circumstances. I do not expect income on it. Stability against inflation is adequate for me. For earing 1% or 2% interest, I shall not part with my gold”.

Rich man’s perspective.

“Holding gold bond takes away the hassle of storing & protecting physical gold”.

5.1.4 Will the bonds be transferable?

This is a Gold Saving A/c.

Hence there won’t be gold bonds. Hence transferability is an issue.

If they don’t give some sort of transferability, the attraction will be less. If transferability is given – it will be better.

(i) Formal transfer to be registered – Good.

(ii) Transferable by delivery - like cash – this will help movement of black money.

5.1.5 This scheme is NOT for black money conversion into white. Depositor has to give KYC.

5.2 Section 115 BBD:

This section provides for concessional tax @ 15% on foreign dividends. Does it constitute an open tap for converting black money into white?

Illustration: IR Pvt. Ltd. is an Indian Resident Private Limited Company. It opens a 100% subsidiary under ODI scheme of FEMA in a Free Trade Zone in UAE. The UAE company makes massive profits, declares dividends and gets money into the country at 15% tax.

Observations: Of course, it is NOT a VDS. There may be people who will be tempted to use S.115 BBD as a VDS. Some of them will cross logical limits. Since no immunity is given, those caught under BML will suffer badly. Similar trends have happened in the past.

5.3 Compare Past Voluntary Disclosure Scheme VDS (1997) with present VCS. VDS # VCS

5.3.1 Under the VDS, people did resort to several schemes and converted black money into white by paying hardly 2% tax.

Consider one of the schemes:

Mr. A would disclose that he had 20 kilos of silver utensils acquired at the time of his marriage – in the year 1972. Silver was purchased

@ Rs. 550 /kg. Cost of silver – Rs. 11,000 was disclosed as his concealed income. He paid tax @ 30% under VDS Rs. 3,300. Then in 1997 he sold silver

utensils @ Rs. 7,000 /kg. & got a cheque of Rs. 1,40,000. Being personal effects, they were not liable to capital gains tax. His tax

cost was 2.35%.

Under the VCS, current market value of the asset has to be considered as tax base. There is no reference to the income from which the undisclosed foreign asset was acquired.

Whether the assessee now sells the asset or not, his tax & penalty amount has been fixed @ 60%. He can’t avoid these.

5.3.2 In the year 1997, even without any game of silver etc., assessees disclosed their incomes under VDS and paid 30% tax. At the same time, normal rate for tax at the highest slab rate was 40%. Very clearly, honest tax payers were at a disadvantage compared to those who used VDS. Under the VCS, tax & penalty together will be 60% of the current market price of the asset. A person using VCS cannot gain advantage over an honest tax payer (who pays tax & surcharge etc. @ 34%).

6. Conclusion or Macro View Final:

Ultimate issue is: “My client should not come into difficulty”.

How do we ensure this?

Best way is, pay up all the taxes that are payable and don’t violate the law.

Next questions are:

CA: “Why should the client come to me for advice and pay me fees?”

Tax Payer: “Government laws are such; and the multiple, varying interpretations by the regulators are such that it is impossible to do any significant business and comply with all the laws.”

“When all my competitors are violating the laws, evading several taxes; how can I remain in competition if I pay all the taxes?”

“Once I evade any indirect tax, black money becomes unavoidable.”

Only answer to those who are still tempted is: “Please look at the breadth & depth of the attack on black money. Do your own Risk Analysis and then decide.”

There have been debates for many decades on following issues. Now Parliament has decided:

(i) There is no difference between Tax Evasion & Tax Avoidance.

(ii) Tax evasion is a crime and will be treated as such.

One may go on debating this. It may be better to realise the facts.

Pranam

Rashmin C. Sanghvi.

Note: For Short Forms used in this paper please see my article on “Black money Law – an Analysis”.